CAPITALlessISM

Reviews

Reviews

Pacific Book Review

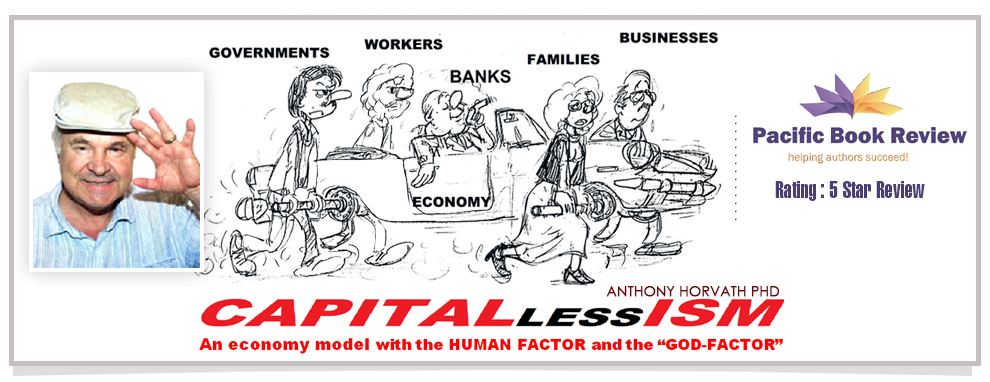

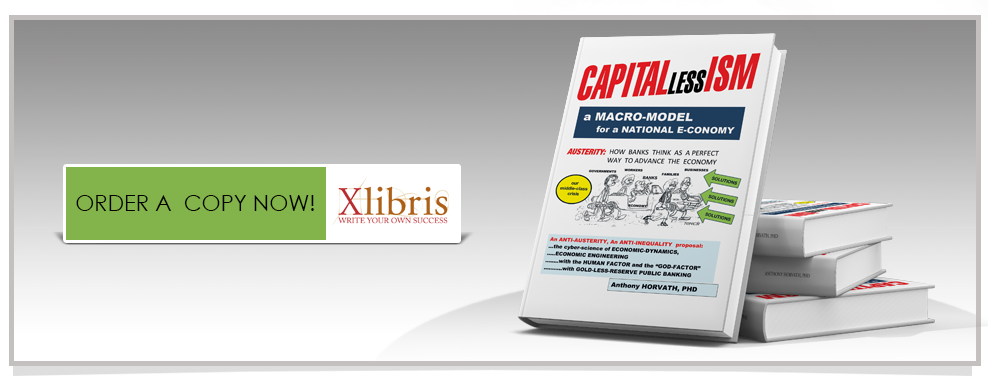

Title: CAPITALlessISM: A Macro-Model for a National E-conomy

Author: Anthony Horvath, PhD

Publisher: XlibrisUS

ISBN: 978-1503554528

Pages: 680

Genre: Business & Economics

Reviewed by: Danita Dyess

Rating: 5 Star Review

With our scientifically and technologically advanced global economy of seven billion people, why do 800 million people go hungry everyday? Why do offshore banks contain accounts for only 1 percent of the people who own 99 percent of the population? In “CAPITALlessISM,” the author Anthony Horvath, Ph.D., interestingly compares our economic system to a biological circulatory system. His premise is simple: Let nature be the prototype for economic engineering.

“CAPITALlessISM” is a mindset of a macro-model for redesigning our inefficient national economy. It is a healthy, free enterprise based model that remedies a lack of capital. It has been practiced by banks using a fractional reserve banking; the process that entails a bank accepting deposits, making loans and holding reserves that are a fraction of its deposits. However, this model takes it one step further. The created mass of E-capital is shared with the government’s own PONC bank, a public-private banking partnership and is ultimately distributed to individuals and entrepreneurs. Although CAPITALlessISM may not be viewed as being politically correct, its controversial ideas attracts dissenters.

The human factor and spiritual God element are fundamental. A pivotal feature is a decrease of inequalities among people and an emphasis on democracy, yet it is not about creating a welfare state nor Communism or Socialism. It is a scientifically designed virtual E-capital resource system. Its e-globalized operations are similar to the bank processes used 300 years ago. Transactions are based between needs and production without reliance on gold (uses kinetic capital like bitcoins).

Horvath vehemently denies being a leftist or an economist. He admits that he did not invent the concepts. Instead, they are an amalgamation of many ideas expressed by Roosevelt, Pope Francis, Gandhi, Mandela and authors of “The Money Masters” which inspired him.

Benefits of “CAPITALlessISM” includes the cancellation of most national debts and life sustaining types of personal debts (medical and educational costs). Options include repayment via the PONC bank or selling them off at fair market value. It would free many nations from high interest payments and austerity programs.

Additionally, a network of national community based cooperative economic systems would be established to reconfigure groups of entrepreneurs according to size; thus creating a cooperative enterprise. PONC bank would manage the operations and entrepreneurs could finance their businesses with their micro-share of their portions (fractional reserve banking). Individual shares would be calculated based on productivity potential. No home equity needed.

Although symbols to depict economic processes, e.g., functions of fluctuation, indicators of continuity, etc. are used, Horvath speaks in layman’s terms. He said, “We are aware that most people are not interested in fancy theories about the economy, let alone the mathematics of it.”

The graphic cover is eye catching and gives a glimpse to the cartoons and anatomical depictions used to capture Horvath’s complex ideas. The 680-page publication book is a combination of three books and offers a methodological approach to reading them. Book one contains an executive summary and overview. Book two discusses the legal grounds for reforms and secrets of free market forces. Book three covers the self sufficient national economy vs. interdependent globalized market economies.

Dr. Anthony Horvath is a former professor at the University of Quebec. He was also a journalist and a consultant. Currently he is the founder of Horvath Research & Development. In 1957, the Hungarian-born immigrant arrived in Canada to escape Communism. As an innovative leader in information system design, he perceives the economy as a huge financial information system.

I found this voluminous work absorbing and holding its posture throughout the explanations and illustrations, a task not easily achieved but done with skill. I would highly recommend “CAPITALlessISM” for anyone who wants to gain an in-depth understanding of his own personal financial standing as well seeking an insight into our nation’s economic engine.

The US Review of Books

CAPITALlessISM: A Macro-Model for a National E-conomy

by Anthony Horvath, PhD

Xlibris

reviewed by John E. Roper

“Freedom implies that ‘capital’ is a privately owned property of someone or some institution, so ‘investors’ are free to dispose of their ‘capital’ as they please. However, this is not so in nature.”

Capitalism has been touted as the dominant and most successful economic model of modern times, yet according to the author the once fair and democratic form of it that helped develop America has been kidnapped by corporatism. But the problem extends far beyond the U.S. borders and has contributed to a worldwide crisis where only a small percentage of the planet’s population are financially well off while the rest struggle under rising debt and looming poverty. In his innovative and thought-provoking book, Horvath puts forward a new economic model, one that can function where no capital is available and that embraces the concept of “community-ism.”

Horvath is the first to admit that his ideas are not completely original. He has been inspired by several sources including Franklin D. Roosevelt’s “Second Bill of Rights,” Thomas Edison’s speculations about a commodity-based currency, and even the human circulatory system. Yet his synthesis of these various models is unique. At its core is the concept of working to eliminate the selfishness and greed that pervades the world’s economies and instead striving toward ways to truly help meet the needs of all people and nations. For example, the International Monetary Fund could be transformed into the International “Mothering” Fund, an organization that would help nations in crisis like a mother nurtures a fetus. And once the nation is again self-sufficient, it won’t slide back into economic instability because it will also not be required to pay back the funds that had been used to rescue it.

Horvath is passionate about his subject, and it shows in his writing. Like a good teacher, he uses a variety of methods such as cartoons, charts, equations, etc. to get his points across. Highly detailed yet very readable, his massive book offers much to think about.

COMMENTS BY DR. ANTHONY HORVATH PUBLISHED BY DR. ELLEN BROWN ON HER WEB.

Ellen Brown, world known author, attorney, speaker, activist has published ten of my comments referring to my book and She has expressed a very favorable opinion about my views on her web.

Ellen Brown is the founder of the Public Banking Institute and the author of a dozen books and hundreds of articles. She developed her research skills as an attorney practicing civil litigation in Los Angeles. In the best-selling Web of Debt, she turned those skills to an analysis of the Federal Reserve and “the money trust.” She showed how this private cartel has usurped the power to create money from the people themselves, and how we the people can get it back.

In The Public Bank Solution, the 2013 sequel, she traces the evolution of two banking models that have competed historically, public and private; and explores contemporary public banking systems globally

Please you can see Ellen Brown publishing my opinions (in blue) on her blog and where I am making a direct reference to my book and our web-site. http://ellenbrown.com/2015/12/11/reinventing-banking-developments-in-russia-iceland-the-uk-and-ecuador/comment-page-1/#comments and you may see her very positive opinion about my comment (in green)

| COMMENTS BY DR. ANTHONY HORVATH PUBLISHED BY DR. ELLEN BROWN ON HER WEB | 1 |

| Ellen Brown, world known author, attorney, speaker, activist has published nine of my comments referring to my book and She has expressed a very favorable opinion about my views on her web. | 1 |

| -1- ON THE TOPIC OF : Reinventing Banking: From Russia to Iceland to Ecuador | 2 |

| Dr. ANTHONY hORVATH, on December 11, 2015 at 12:24 pm said: | 3 |

| Dr. ELLEN BROWN’S FAVORABLE RESPONSE to my comment | 3 |

| Dr. ANTHONY hORVATH, on January 9, 2016 at 12:04 pm said: | 4 |

| Dr. ANTHONY hORVATH, on December 13, 2015 at 8:08 pm said: | 4 |

| Dr. ANTHONY hORVATH, on December 14, 2015 at 8:47 am said: | 5 |

| Dr. ANTHONY hORVATH, on January 9, 2016 at 7:51 pm said: | 6 |

| Dr. ANTHONY hORVATH, on December 14, 2015 at 3:28 pm said: | 7 |

| -2- ON THE TOPIC OF : How to eliminate income taxes and the federal debt: by presidential candidate Scott Smith on “It’s Our Money” | 8 |

| Dr. ANTHONY hORVATH, on December 11, 2015 at 12:11 pm said: | 8 |

| -3- ON THE TOPIC OF : A Crisis Worse than ISIS? Bail-Ins Begin… | 9 |

| Dr. ANTHONY hORVATH, on January 4, 2016 at 9:04 pm said: | 9 |

| -4- ON THE TOPIC OF : Les Leopold on “It’s Our Money” | 10 |

| Dr. ANTHONY hORVATH, on January 10, 2016 at 9:25 pm said: | 11 |

| Dr. ANTHONY hORVATH, on January 13, 2016 at 9:02 am said: | 12 |

-1- ON THE TOPIC OF : Reinventing Banking: From Russia to Iceland to Ecuador

Posted on December 11, 2015 by Ellen Brown

Global developments in finance and geopolitics are prompting a rethinking of the structure of banking and of the nature of money itself. Among other interesting news items:

- In Russia, vulnerability to Western sanctions has led to proposals for a banking system that is not only independent of the West but is based on different design principles.

- In Iceland, the booms and busts culminating in the banking crisis of 2008-09 have prompted lawmakers to consider a plan to remove the power to create money from private banks.

- In Ireland, Iceland and the UK, a recession-induced shortage of local credit has prompted proposals for a system of public interest banks on the model of the Sparkassen of Germany.

- In Ecuador, the central bank is responding to a shortage of US dollars (the official Ecuadorian currency) by issuing digital dollars through accounts to which everyone has access, effectively making it a bank of the people.

Developments in Russia

In a November 2015 article titled “Russia Debates Unorthodox Orthodox Financial Alternative,” William Engdahl writes:

A significant debate is underway in Russia since imposition of western financial sanctions on Russian banks and corporations in 2014. It’s about a proposal presented by the Moscow Patriarchate of the Orthodox Church. The proposal, which resembles Islamic interest-free banking models in many respects, was first unveiled in December 2014 at the depth of the Ruble crisis and oil price free-fall. This August the idea received a huge boost from the endorsement of the Russian Chamber of Commerce and Industry. It could change history for the better depending on what is done and where it further leads.

Engdahl notes that the financial sanctions launched by the US Treasury in 2014 have forced a critical rethinking among Russian intellectuals and officials. Like China, Russia has developed an internal Russian version of SWIFT Interbank payments; and it is now considering a plan to restructure Russia’s banking system. Engdahl writes:

Much as with Islamic banking models that ban usury, the Orthodox Financial System would not allow interest charges on loans. Participants of the system share risks, profits and losses. Speculative behavior is prohibited . . . . There would be a new low-risk bank or credit organization that controls all transactions, and investment funds or companies that source investors and mediate project financing. . . . Priority would be ensuring financing of the real sector of the economy . . . .

On September 15, 2013, Sergei Glazyev, one of Vladimir Putin’s economic advisers,presented a a series of economic proposals to the Presidential Russian Security Council that also suggest radical change is on the horizon. The plan is aimed at reducing vulnerability to western sanctions and achieving long-term growth and economic sovereignty.

Particularly interesting is a proposal to provide targeted lending for businesses and industries by providing them with low-interest loans at 1-4 percent, financed through the central bank with quantitative easing (digital money creation). The proposal is to issue 20 trillion rubles for this purpose over a five year period. Using quantitative easing for economic development mirrors the proposal of UK Labour Leader Jeremy Corbyn for “quantitative easing for people.”

William Engdahl concludes that Russia is in “a fascinating process of rethinking every aspect of her national economic survival because of the reality of the western attacks,” one that “could produce a very healthy transformation away from the deadly defects” of the current banking model.

Iceland’s Radical Money Plan

Iceland, too, is looking at a radical transformation of its money system, after suffering the crushing boom/bust cycle of the private banking model that bankrupted its largest banks in 2008. According to a March 2015 article in the UK Telegraph:

Iceland’s government is considering a revolutionary monetary proposal – removing the power of commercial banks to create money and handing it to the central bank. The proposal, which would be a turnaround in the history of modern finance, was part of a report written by a lawmaker from the ruling centrist Progress Party, Frosti Sigurjonsson, entitled “A better monetary system for Iceland”.

“The findings will be an important contribution to the upcoming discussion, here and elsewhere, on money creation and monetary policy,” Prime Minister Sigmundur David Gunnlaugsson said. The report, commissioned by the premier, is aimed at putting an end to a monetary system in place through a slew of financial crises, including the latest one in 2008.

Under this “Sovereign Money” proposal, the country’s central bank would become the only creator of money. Banks would continue to manage accounts and payments and would serve as intermediaries between savers and lenders. The proposal is a variant of the Chicago Plan promoted by Kumhof and Benes of the IMF.

Public Banking Initiatives in Iceland, Ireland and the UK

A major concern with stripping private banks of the power to create money as deposits when they make loans is that it will seriously reduce the availability of credit in an already sluggish economy. One solution is to make the banks, or some of them, public institutions. They would still be creating money when they made loans, but it would be as agents of the government; and the profits would be available for public use, on the model of the US Bank of North Dakota and the German Sparkassen (public savings banks).

In Ireland, three political parties – Sinn Fein, the Green Party and Renua Ireland (a new party) — are now supporting initiatives for a network of local publicly-owned banks on the Sparkassen model. In the UK, the New Economy Foundation (NEF) is proposing that the failed Royal Bank of Scotland be transformed into a network of public interest banks on that model. And in Iceland, public banking is part of the platform of a new political party called the Dawn Party.

Ecuador’s Dinero Electronico: A National Digital Currency

So far, these banking overhauls are just proposals; but in Ecuador, radical transformation of the banking system is under way.

Ever since 2000, when Ecuador agreed to use the US dollar as its official legal tender, it has had to ship boatloads of paper dollars into the country just to conduct trade. In order to “seek efficiency in payment systems [and] to promote and contribute to the economic stability of the country,” the government of President Rafael Correa has therefore established the world’s first national digitally-issued currency.

Unlike Bitcoin and similar private crypto-currencies (which have been outlawed in the country), Ecuador’s dinero electronico is operated and backed by the government. The Ecuadorian digital currency is less like Bitcoin than like M-Pesa, a private mobile phone-based money transfer service started by Vodafone, which has generated a “mobile money” revolution in Kenya.

Western central banks issue digital currency for the use of commercial banks in their reserve accounts, but it is not available to the public. In Ecuador, any qualifying person can have an account at the central bank; and opening one is as easy as walking into a participating financial institution and exchanging paper money for electronic money stored on their smartphones.

Ecuador’s banks and other financial institutions were ordered in May 2015 to adopt the digital payment system within the next year, making them “macro-agents” of the Electric Currency System.

According to a National Assembly statement:

Electronic money will stimulate the economy; it will be possible to attract more Ecuadorian citizens, especially those who do not have checking or savings accounts and credit cards alone. The electronic currency will be backed by the assets of the Central Bank of Ecuador.

That means there is no fear of the bank going bankrupt or of bank runs or bail-ins. Nor can the digital currency be devalued by speculative short selling. The government has declared that these are digital US dollars trading at 1 to 1 – take it or leave it – and the people are taking it. According to an October 2015 article titled “Ecuador’s Digital Currency Is Winning Hearts!”, the currency is actually taking the country by storm; and other countries in Latin America and Africa are not far behind.

The president of the Ecuadorian Association of Private Banks observes that the digital currency could be used to finance the public debt. However, the government has insisted that this will not be done. According to an economist at Ecuador’s central bank:

We did it from the government because we wanted it to be a democratic product. In any other countries, [digital currency] is provided by private companies, and it is expensive. There are barriers to entry, like [expensive fees] if you transfer money from one cellphone operator to another. What we have here is something everyone can use regardless of the operator they are using.

Banking Moves into the 21st Century

The catastrophic failures of the Western banking system mandate a new vision. These transformations, current and proposed, are constructive steps toward streamlining the banking system, eliminating the risks that have devastated individuals and governments, democratizing money, and promoting sustainable and prosperous economies.

They also raise some provocative questions:

My COMMENTS…

Dr. ANTHONY hORVATH, on December 11, 2015 at 12:24 pm said:

thank God that several other authors think the same way!!!!!!!

I abound and quote your works in my book, a 680 page study

title :CAPITALlessISM, a MACRO-MODEL for a NATIONAL ECONOMY,by Dr. Anthony Horvath

So how could we reverse the crisis?

By financing the economy

è ==> using a new concept: with a NATIONALIZED artificial capital creation process, called “FRACTIONAL RESERVE BANKING’’ rights, then FRANCHISING it back to the BANKS… thus eliminating income taxes

è ==> using a PUBLIC-PRIVATE COOPERATIVE BANKING NETWORK PARTNERSHIP UNDER GOVERNMENT COORDINATION

è ==> REEVALUATING OR CHALLENGING THE VALIDITY OF NATIONAL DEBTS ON LEGAL GROUNDS

all explained in my book ….. I would be happy to publish on your site

Dr. ELLEN BROWN’S FAVORABLE RESPONSE to my comment

Ellen Brown, on December 12, 2015 at 3:38 pm said:

Interesting! That’s my vision as well. It’s also Scott Smith’s, the presidential candidate I just interviewed. See previous post. Thanks!

My comments to Ellen Brown’s radio interview with independent presidential candidate Scott Smith

http://prn.fm/its-our-money-with-ellen-brown-addressing-a-digital-divide-12-09-15/

Dr. ANTHONY hORVATH, on January 9, 2016 at 12:04 pm said:

dear Dan…. from Dr. Anthony Horvath, author of CAPITALlessISM….. https://capitallessism.com/ …..-1- the present private banking structure has to evolve into a Public-Private banking system… in harmony… -2- the present artificial capital creation process under private banks control, must become a public property licensed back to them. -3- the size of National debts must be reevaluated under certain new legalities. -4- Economy work with only with people in mind… the HUMAN FACTOR …. -5- Durable economic reforms may be achieved only peacefully with a certain elusive god-factor … without revolutions.

Dr. ANTHONY hORVATH, on December 13, 2015 at 8:08 pm said:

CAPITALlessISM, a MACRO-MODEL for a NATIONAL E-CONOMY,

by Dr. Anthony Horvath a 680 page study http://www.capitallessism (goggle)

Ecuador’s National Digital Currency system is the future model for a stable national E-CONOMY under a NATIONAL PUBLIC BANKING, where presently foreign bank controlled currency supply dominate the fluctuating trade. To insure stability (where there is a balance between production capacity and the survival consumerism capacity) the money supply has to be nationally created, distributed, its circulation monitored with precision in order to sustain balance. In our book, we envisioned the creation of such an E-conomy, i.e. a national electronic currency supply consisting of CMMs, Currency Movement Monitoring system, ‘BIT-BILL®, E-cash, E-bank concepts, E-cash, E-wallet, and piracy-proof virtual currency designs. The goal is to create an adequate currency supply, to stimulate its circulation, and to monitor its usage … and also to discourage counterfeiting and corruption

Reply

Lise, on December 14, 2015 at 5:34 am said:

Dr. Anthony …. why is it that the money supply has to be nationally created ? Why can’t the market participate in creating money supply that is of an asset origin and debt-free ?

Dr. ANTHONY hORVATH, on December 14, 2015 at 8:47 am said:

thank you for your very interesting question, …. national control over money supply creation should be a national process vs a privatized priviledge SOLELY UNDER the jurisdiction of private banks.

For two simple reasons :

-1- First, that governments, at least in principle, have an OVERALL assessment of the GLOBAL CAPITAL needs of the people, institutions and enterprises, while ”market interests” have only a FRACTIONAL view of these same needs. Consequently, governments must also have the corresponding OVERALL CAPITAL CREATION CAPACITY to sustain these needs in a nation. On the other hand, since ”market assessment of these same needs” are only a FRACTIONAL view of global human needs, (because they are biased by private interests from their own profitability perspective), they should also have at best, only a FRACTIONAL CAPITAL CREATION CAPACITY along with democratic governments. While profit perspectives are most important in a free enterprise society, they are nevertheless useless to determine the capital needs of non-profit oriented services.

-2- The second reason is that asset-based credit creation process is too restricitive. It presupposes that marketable assets exist already on which to consent a credit i.e. for new-capital. So in the absence of sufficient assets, it becomes too restrictive to the full development potential of those projects that cannot show an asset to obtain capital. So, because sufficient e-capital cannot be created by the traditional asset based ”market-oriented” virtual capital creation process we need innovative E-CAPITAL CREATIONS DESCRIBED IN OUR BOOK: CAPITAL-less-ISM, a MACRO-MODEL for a NATIONAL E-CONOMY.

this is why we suggest a NATIONAL FRACTIONAL RESERVE BANKING PROCESS, FRANCHISED TO PRIVATE BANKS BY GOVERNMENTS, under the jurisdiction of NATIONAL PUBLIC BANKS.

thank you for comments

Lise, on January 9, 2016 at 11:50 am said:

Dr. Anthony …. Where did you ever get the idea that asset based currency is too restrictive ? How can that statement be justified ?

Dr. ANTHONY hORVATH, on January 9, 2016 at 7:51 pm said:

Dear Lise …..thank you….. from Dr. Anthony Horvath, author of CAPITALlessISM.. https://capitallessism.com/

Originally, currency creation processes were based on gold reserves. i.e. the amount of currency issued were limited (restricted) by gold assets. i.e. the paper currency was equivalent to the gold reserves. Since this proved insufficient to produce enough ‘’paper’’ capital to sustain the war efforts of opposing nations, the concept of fractional reserve banking was introduced by banks in order to issue much more paper/credit capital than covered by the gold reserves. (… presently over 100 new virtual artificial dollars are issued for each one in the reserve…). But, today this process is still insufficient to cover the hyper-exponentially growing development-capital needs of the exponentially growing world population. This is a MATHEMATICAL EVIDENCE … so emerging nations need new capital creation concepts, instead of begging foreign investors for no-existent capital. So, ‘’asset based currency creation’’ seems to be outdated.

Consequently, we recommend in our book CAPITALlessISM ….that -1- the present private banking structure has to evolve into a Public-Private banking system… in harmony(not nationalized as leftists advocate) -2- the present artificial capital creation process under private banks’ control, must become a public property licensed back to them. So the new virtual-capital created should be a commodity based and a production potential based (not gold-reserve based) NATIONAL property -3- the size of National debts must be re-evaluated under certain new legalities. -4- Economy can work only with people and family needs in mind… the HUMAN FACTOR …. -5- DURABLE economic reforms can be achieved only PEACEFULLY with a certain elusive god-factor … without revolutions and the present RADICALIZATION TENDENCY.

thank you for your comments

Dr. ANTHONY hORVATH, on December 14, 2015 at 3:28 pm said:

thank you Lise, for your very interesting question, …. national control over money supply creation should be a national process vs a privatized priviledge SOLELY UNDER the jurisdiction of private banks.

For two simple reasons :

-1- First, that governments, at least in principle, have an OVERALL assessment of the GLOBAL CAPITAL needs of the people, institutions and enterprises, while ”market interests” have only a FRACTIONAL view of these same needs. Consequently, governments must also have the corresponding OVERALL CAPITAL CREATION CAPACITY to sustain these needs in a nation. On the other hand, since ”market assessment of these same needs” are only a FRACTIONAL view of global human needs, (because they are biased by private interests from their own profitability perspective), they should also have at best, only a FRACTIONAL CAPITAL CREATION CAPACITY along with democratic governments. While profit perspectives are most important in a free enterprise society, they are nevertheless useless to determine the capital needs of non-profit oriented services.

-2- The second reason is that asset-based credit creation process is too restricitive. It presupposes that marketable assets exist already on which to consent a credit i.e. for new-capital. So in the absence of sufficient assets, it becomes too restrictive to the full development potential of those projects that cannot show an asset to obtain capital. So, because sufficient e-capital cannot be created by the traditional asset based ”market-oriented” virtual capital creation process we need innovative E-CAPITAL CREATIONS DESCRIBED IN OUR BOOK: CAPITAL-less-ISM, a MACRO-MODEL for a NATIONAL E-CONOMY.this is why we suggest a NATIONAL FRACTIONAL RESERVE BANKING PROCESS, FRANCHISED TO PRIVATE BANKS BY GOVERNMENTS, under the jurisdiction of NATIONAL PUBLIC BANKS.

thank you for comments

Reinventing Banking: From Russia to Iceland to Ecuador – Thought Crime Radio, onDecember 13, 2015 at 9:46 pm said:

[…] http://ellenbrown.com/2015/12/11/reinventing-banking-developments-in-russia-iceland-the-uk-and-ecuad…

-2- ON THE TOPIC OF : How to eliminate income taxes and the federal debt: by presidential candidate Scott Smith on “It’s Our Money”

How to eliminate income taxes and the federal debt: Scott Smith on “It’s Our Money” | State of Globe, on December 14, 2015 at 5:38 am said:

…. items of interest on “It’s Our Money” this week, Ellen Brown interviewed Independent presidential candidate Scott Smith, who has a clever plan for eliminating austerity, income taxes and the federal debt without creating inflation.

Dr. ANTHONY hORVATH, on December 11, 2015 at 12:11 pm said:

CONGRATULATIONS !!!!!!!! I share totally your views with my new book published a month ago

”CAPITALlessISM, a MACRO-MODEL for a NATIONAL ECONOMY”

author, ANTHONY HORVATH PHD.

An ANTI-AUSTERITY, and an ANTI-INEQUALITY proposal:

…ECONOMIC-DYNAMICS, the science of cybernetic capital flow

…..ECONOMIC ENGINEERING , its mathematical application

……..with the HUMAN FACTOR and the “GOD-FACTOR”

………..within a new PUBLIC-PRIVATE BANKING SYSTEM 514-867-2272

-3- ON THE TOPIC OF : A Crisis Worse than ISIS? Bail-Ins Begin…

Posted on December 29, 2015 by Ellen Brown

While the mainstream media focus on ISIS extremists, a threat that has gone virtually unreported is that your life savings could be wiped out in A MASSIVE DERIVATIVES COLLAPSE. BANK BAIL-INS HAVE BEGUN IN EUROPE, and the infrastructure is in place in the US. Poverty also kills.

At the end of November, an Italian pensioner hanged himself after his entire €100,000 savings were confiscated in a bank “rescue” scheme. He left a suicide note blaming the bank, where he had been a customer for 50 years and had invested in bank-issued bonds. …..

http://www.thelocal.it/20151211/italy-moves-to-bail-out-savers-hit-by-bank-plan

The €3.6 billion ($3.83 billion) rescue plan launched by the Italian government uses a newly-formed National Resolution Fund, which is fed by the country’s healthy banks. But before the fund can be tapped, losses must be imposed on investors; and in January, EU rules will require that they also be imposed on depositors. According to a December 10th article on BBC.com:

Dr. ANTHONY hORVATH, on January 4, 2016 at 9:04 pm said:

Dear Ellen Brown…!!! public banking is the answer as you advocate it.

HOW TO PREVENT BAIL-INS, or BANKS TAKING OUR SAVINGS?

please read . in CAPITALlessISM by Dr. Anthony Horvath

https://capitallessism.com/

By reinventing the entire banking industry and by reinventing a new type of national currency (for circulation to link population needs to production capabilities in the nation) …. This can be done with a new public-private-cooperative banking structured network .. and by reinventing Edison’s commodity based currency … based not gold reserves but on commodities and production potential,( instead of the bank owned dollar). This new virtual currency system is similar to a national E-voucher system (activated through a wireless cell-system), outside of the present legal jurisdiction of private banks. This new E-cash currency system could be developed similar to a gigantic virtual barter system. So instead of private banks, we will have APPLE-BANK or GOOGLE BANK administering it under government supervision, Your personal production potential, could be linked up to an employment potential, linked up to a e-cash issued to you to sustain your survival consumer needs.

Thank you for your comments back.

Dr. ANTHONY hORVATH, on January 4, 2016 at 9:04 pm said:

Dear Ellen Brown…!!! public banking is the answer as you advocate it.

HOW TO PREVENT BAIL-INS, or BANKS TAKING OUR SAVINGS?

please read . in CAPITALlessISM by Dr. Anthony Horvath

https://capitallessism.com/

By reinventing the entire banking industry and by reinventing a new type of national currency (for circulation to link population needs to production capabilities in the nation) …. This can be done with a new public-private-cooperative banking structured network .. and by reinventing Edison’s commodity based currency … based not gold reserves but on commodities and production potential,( instead of the bank owned dollar). This new virtual currency system is similar to a national E-voucher system (activated through a wireless cell-system), outside of the present legal jurisdiction of private banks. This new E-cash currency system could be developed similar to a gigantic virtual barter system. So instead of private banks, we will have APPLE-BANK or GOOGLE BANK administering it under government supervision, Your personal production potential, could be linked up to an employment potential, linked up to a e-cash issued to you to sustain your survival consumer needs.

Thank you for your comments back.

-4- ON THE TOPIC OF : Les Leopold on “It’s Our Money”

http://ellenbrown.com/2016/01/10/les-leopold-on-its-our-money/#comments

Posted on January 10, 2016 by Ellen Brown

Founder of the Labor Institute, Les Leopold, about how the market mechanics of inequality have succeeded over the past 40 years and what we can do collectively to bring about real change. She also discusses her latest article about the looming crisis that could be triggered by the new practice of bailing-in depositor money to save failing banks. And Matt Stannard delivers some words about money from the mouths of historical figures. Listen to the archive here.

Dr. ANTHONY hORVATH, on January 10, 2016 at 9:25 pm said:

dear Ellen and Leopold … I love your ideas

from Dr. Anthony Horvath, author of CAPITALlessISM…..

https://capitallessism.com/

the ANTI-BANKS …. A PREVENTIVE ANTIDOTE TO THE DANGERS OF BAIL-INS : a mas effort to establish jointly a PUBLIC COMMUNITY BANKING network with many COOPERATIVE CREDIT UNIONS also with the ENCOURAGEMENT OF CHURCHES COMMUNITIES. we discuss these issues in my book.

WHY…? THE AMERICAN DREAM IS DEAD! THE MIDDLE CLASS HAS TOTALLY ERODED TO BECOME THE NEW SLAVE CLASS.

Since the Communist economic vision has collapsed, the ultra-capitalist-corporatism forces dominate the economy and the middle class collapsed. Economy has become too complicated for most of us to understand. The FREE and FAIR, DEMOCRATIC CAPITALISM that has developed America has been kidnapped by CORPORATISM. What is it? It is a radical fundamentalist form of ultra-capitalism. CORPORATISM is the privatization of a Communist-state-styled economic dictatorship by corporations.

A LIVE EXAMPLE : In Quebec, as an antidote to the dominance of banks during the depression years of the 1930-s contributed to the economic awareness of the population to seek alternative solutions. PUBLIC COOPERATIVE COMMUNITY BANKS… called CAISSE POPULAIRES. Under the Church’ spiritual authority seventy-five years ago in church basements people started the movement Desjardins, a cooperative community banking system. People gathered to discuss economic issues, such as financing enterprises, home financing, put their meager savings together etc. The result was the astonishing new concept of forming community cooperative credit unions. With the church’s encouragement, in a short seventy-six years, Quebec has built up several economic giants: Quebec’s Caisse Populaire Desjardins, a financial cooperative movement, valued at over $220 billion (among the world largest banking institutions) and the Caisse de Depot et Placement, valued at over $150 billion. Add also, the Bank National and the Laurentian Bank, as well as the investment capital Fond de Solidarité. Add over all these, a cooperative concept for a vast network of small and medium size enterprises, with its ramifications in many sectors of the economy. Quebec has the most elaborate cooperative system in the world.

So yes, people can do fantastic achievements collectively when they become aware of a commune danger. If I add the huge technical potential of the social networks …. we might have new financial institutions in short months like UBER-BANKS to counter traditional banks or like like APPLE-BANKS …. GOOGLE-BANKS …. a determined community may very well prevent bail-ins….

Thank you for your feedback

Dr. ANTHONY hORVATH, on January 13, 2016 at 9:02 am said:

dear R A FEIBEL and Johnraymondnolan, … yes, THERE IS HOPE!!!

From Dr. Anthony Horvath, author of CAPITALlessISM…..

https://capitallessism.com/

your descriptions of apocalyptic views of the economy are very real indeed and it is a wake-up call to all of us. We have all become too comfortable with the idea that from cradle-to-grave a good uncle Sam’s ”American way” will automatically take care of us and flourish our culture. Well. we cannot take it for granted !!!. …but only, a COLLECTIVE COMMUNITY TYPE AWARENESS is the beginning to react to these dangers.. It is the key. Thank God, for social media… our education level, instant information availability and human ingenuity… and an elusive ”GOD-FACTOR”. THE REST will come slowly by itself: PUBLIC-BANKING, COOPERATIVE ENTREPRENEURSHIP, COMMUNITY-SPIRIT OF MUTUAL NEIGHBORING HELP .under the guidance of our two thousand year old Judaeo-Christian Heritage. In ”CAPITALlessISM…..” we discuss the deep long-term effect of a CERTAIN ”GOD-FACTOR” ON THE ECONOMY.

Every economic-military dictatorship in history have collapsed under this mysterious ”God-factor” and under the ingenious human resistance awareness reactions :… the Roman-Empire, the Ottoman Empire, the British colonialism in India (with Gandhi), in Africa (with Nelson Mandela), Communism ….. But what took centuries because of the poor communication technologies and illiterate masses of people at the time might take only only a very short generation to react to these new forms of economic dictatorship.

WELL, I HOPE SO AT LEAST …. thank you for your comments